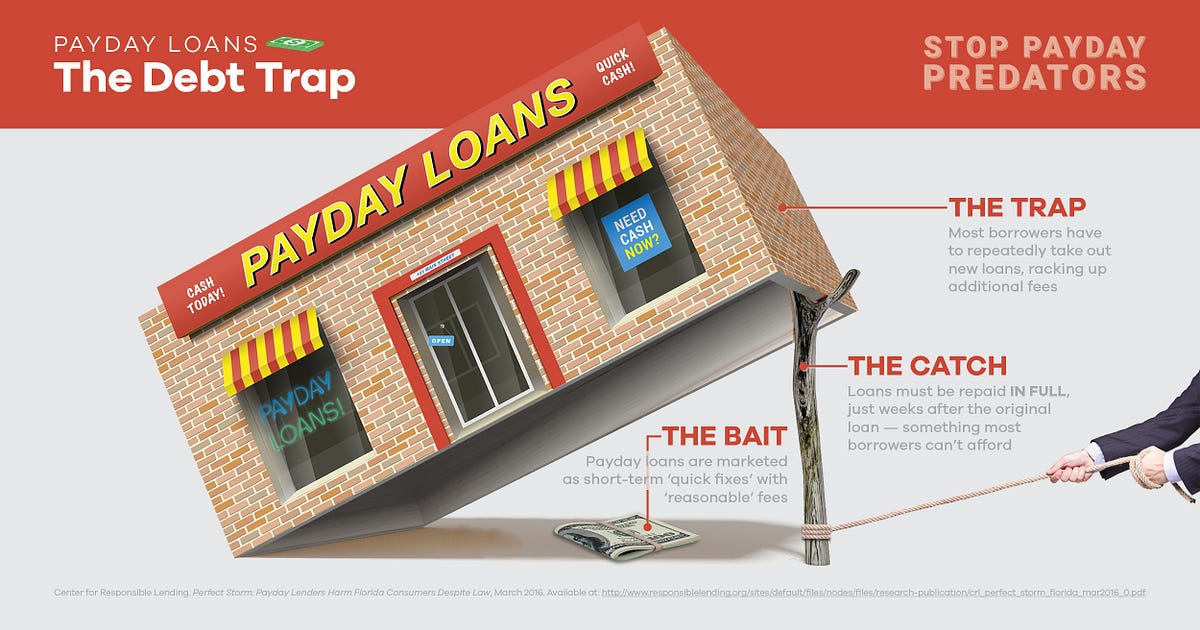

Payday loans may offer immediate cash relief but can quickly become a debt trap. High fees and interest rates often lead to a cycle of borrowing that is hard to escape.

Payday loans promise quick cash for urgent financial needs, making them attractive to many. However, the hidden costs can turn these loans into a financial nightmare. Borrowers often face exorbitant interest rates, leading to a cycle of debt that keeps them borrowing just to stay afloat.

Many find themselves trapped, unable to pay off the original loan without taking out another. Understanding the risks associated with payday loans is crucial for making informed financial decisions. This article explores whether payday loans serve as a quick fix or ultimately become a damaging debt trap.

The Allure Of Payday Loans

Payday loans attract many people seeking quick cash. They promise immediate financial relief without lengthy processes. This appeal often overshadows the risks involved. Understanding the allure helps in making informed decisions.

Immediate Financial Relief

For those facing unexpected expenses, payday loans offer a fast solution. Here are some reasons why they seem appealing:

- Quick access to cash: Funds are often available within hours.

- No credit checks: Many lenders do not require a credit history.

- Simple application process: Most applications are straightforward and easy to complete.

This immediate access can be tempting. For example, a car repair or medical bill may need urgent payment. Borrowers often feel that a payday loan is their only option. They believe this quick fix will solve their problems.

The Promise Of A Quick Fix

Payday loans market themselves as the ultimate quick fix. Lenders emphasize their convenience and speed. Many borrowers overlook the important details:

- High interest rates: Rates can exceed 400% annually.

- Short repayment periods: Most loans are due within two weeks.

- Risk of debt cycle: Borrowers may need to take out new loans to pay old ones.

This cycle can lead to financial strain. The initial relief often turns into a burden. Understanding these factors is crucial before borrowing.

Credit: medium.com

Understanding The Basics

Payday loans often appear as a quick solution to urgent financial needs. However, understanding their fundamentals is crucial. Many people overlook the risks associated with these loans. This section delves into how payday loans operate and their associated costs.

How Payday Loans Work

Payday loans are short-term loans designed to cover immediate expenses. They typically have a repayment period of two to four weeks. Here’s a simple overview:

- Borrowers apply for a specific amount.

- Lenders often require proof of income.

- Loan amounts vary, usually ranging from $100 to $1,000.

- Loan repayment coincides with the borrower’s next paycheck.

Most lenders require access to the borrower’s bank account. This allows them to withdraw the loan amount plus fees on the due date. Failure to repay can lead to severe consequences.

Fixed Fees And Interest Rates

Payday loans typically feature fixed fees. These fees are often very high compared to traditional loans. Here’s a breakdown:

| Loan Amount | Typical Fee | APR (Annual Percentage Rate) |

|---|---|---|

| $100 | $15-$30 | 390%-780% |

| $500 | $75-$100 | 390%-780% |

The high APR makes payday loans expensive. Borrowers may end up paying much more than they borrowed. This cycle can trap individuals in ongoing debt.

Deceptive Ease And Accessibility

Payday loans appear simple to obtain. They promise quick cash without the usual hurdles. This ease often masks serious financial risks. Many borrowers find themselves trapped in a cycle of debt.

No Collateral Required

One major attraction of payday loans is that they require no collateral. Borrowers do not need to risk personal property. This makes them appealing for people without assets. However, this lack of collateral comes with high costs.

Without collateral, lenders charge exorbitant interest rates. Many borrowers underestimate these fees. A small loan can quickly spiral into a large debt.

Online Applications And Instant Approvals

Most payday lenders offer online applications. This convenience allows borrowers to apply from home. Many lenders promise instant approvals, making it feel effortless.

However, quick approvals often lead to rushed decisions. Borrowers may not fully understand the terms. This can lead to borrowing more than needed.

| Feature | Pros | Cons |

|---|---|---|

| No Collateral | Easy access for those without assets | High interest rates |

| Online Applications | Convenient and fast | Possible rushed decisions |

| Instant Approvals | Quick cash availability | Hidden fees and terms |

Understanding these features is crucial. Borrowers must consider the long-term impact. Quick cash may not be worth the potential debt trap.

Credit: qsalary.com

The Debt Spiral Begins

Payday loans often seem like a quick solution for urgent cash needs. Many people face unexpected expenses and feel trapped. They may borrow money without understanding the consequences. The cycle of borrowing can quickly turn into a dangerous debt spiral.

Short-term Solutions, Long-term Problems

Payday loans provide immediate cash. However, they come with severe downsides:

- High interest rates

- Short repayment terms

- Risk of additional fees

These loans may seem beneficial at first. Yet, they lead to long-term financial struggles. Borrowers often find themselves in a bind, needing to take out new loans to pay off old ones.

The Cycle Of Borrowing And Debt

This cycle can look like this:

- Borrow money through a payday loan.

- Struggle to repay the loan on time.

- Take out another loan to cover the first.

- Repeat the cycle, accumulating more debt.

The result? A debt spiral that feels impossible to escape. Many borrowers end up trapped in a continuous loop of borrowing, leading to financial ruin.

Consequences Of Non-payment

Payday loans can seem like a quick solution for immediate cash needs. However, non-payment can lead to serious consequences. Understanding these impacts is crucial for responsible borrowing.

Legal Actions And Collections

Failure to repay a payday loan can trigger severe legal actions. Lenders often pursue collections aggressively. Here are some potential outcomes:

- Collections Agency Involvement: Lenders may sell your debt to a collections agency.

- Legal Action: Lenders can sue you for the unpaid amount.

- Wage Garnishment: Courts may allow lenders to take money from your paycheck.

These actions can add substantial stress. Legal fees and additional costs can increase your debt significantly.

Impact On Credit Scores

Not repaying a payday loan can severely harm your credit score. A lower credit score affects future borrowing options.

| Credit Score Range | Impact Level |

|---|---|

| 300 – 579 | Very Poor |

| 580 – 669 | Fair |

| 670 – 739 | Good |

| 740 – 799 | Very Good |

| 800 – 850 | Excellent |

Even one missed payment can drop your score. A lower score means higher interest rates on future loans. This cycle can trap you in debt.

The High Cost Of Quick Cash

Payday loans may seem like a quick solution for urgent cash needs. However, they come with serious risks. Understanding the costs involved is crucial. Many borrowers find themselves trapped in a cycle of debt. The high expenses can turn a small loan into a financial nightmare.

Exorbitant Interest Rates

Payday loans often carry outrageous interest rates. These rates can reach up to 400% APR or more. This means that a small loan can cost you significantly over time. Here’s a quick breakdown:

| Loan Amount | Interest Rate | Total Repayment |

|---|---|---|

| $100 | 400% | $500 |

| $200 | 400% | $1,000 |

| $500 | 400% | $2,500 |

Many borrowers underestimate these costs. They think they can pay it back quickly. But the high interest can trap them in debt.

Hidden Fees And Penalties

Payday loans come with hidden fees and penalties. Borrowers often overlook these extra costs. Here are some common hidden charges:

- Origination fees

- Late payment fees

- Check processing fees

- Early repayment penalties

These fees add up quickly. They can make a manageable loan unmanageable. Borrowers should read the fine print carefully. Understanding all potential costs can prevent financial trouble.

In summary, payday loans can be a quick fix but often lead to a debt trap. The high costs associated with these loans can create long-term financial issues.

Alternatives To Payday Loans

Payday loans may seem like an easy solution for urgent cash needs. However, they can lead to overwhelming debt. Exploring alternatives can provide safer financial options. Here are some effective alternatives to consider.

Credit Unions And Small Loans

Credit unions offer small loans with lower interest rates. They often have more flexible terms than payday lenders. Here are some benefits:

- Lower Interest Rates: Rates are significantly lower than payday loans.

- Personalized Service: Credit unions focus on member needs.

- Financial Education: Many offer budgeting and financial planning resources.

Consider a small loan from a local credit union. Compare their rates and terms with payday loans. This can help avoid the debt cycle associated with high-interest loans.

Budgeting And Emergency Funds

Creating a budget is essential for managing finances. It helps track spending and saves money. Here are some tips:

- Track Expenses: Write down all monthly expenses.

- Set Savings Goals: Aim to save a specific amount each month.

- Build an Emergency Fund: Save at least three to six months of expenses.

Emergency funds can cover unexpected costs without relying on loans. Start small. Even saving $10 a week can add up. Over time, this can provide a financial cushion.

Breaking Free From The Debt Trap

Payday loans offer quick cash but often lead to a cycle of debt. Many people find themselves trapped, struggling to pay back the loan. Breaking free requires effective strategies and support. Understanding debt management is crucial for recovery.

Debt Management Strategies

Implementing solid debt management strategies can help regain control. Here are some effective methods:

- Create a budget: Track income and expenses. Identify areas to cut back.

- Prioritize debts: Focus on high-interest loans first. Pay minimums on others.

- Negotiate with lenders: Discuss lower payments or extended terms. Many lenders are willing to help.

- Consider debt consolidation: Combine multiple loans into one. This can lower monthly payments.

- Build an emergency fund: Save small amounts regularly. This helps avoid future loans.

Seeking Professional Financial Advice

Professional financial advice can provide valuable insights. Experts offer guidance tailored to individual situations. Consider the following options:

| Type of Advice | Description |

|---|---|

| Credit Counseling | Helps create a personalized budget plan. |

| Financial Planning | Offers long-term strategies for financial health. |

| Debt Management Programs | Consolidates debts into manageable monthly payments. |

Finding the right advisor is essential. Look for certified professionals. Ensure they have experience with payday loans and debt recovery.

Frequently Asked Questions

Are Payday Loans Good Or Bad Debt?

Payday loans are generally considered bad debt. They come with high interest rates and fees, making repayment difficult. This can lead to a cycle of debt, worsening financial situations. For short-term needs, exploring alternatives is often a better choice.

What Happens If You Can’t Pay Back A Payday Loan?

Failing to repay a payday loan can lead to severe consequences. Lenders may send your account to collections, resulting in legal action. Expect high fees and potential damage to your credit score. Seeking financial advice can help manage the situation effectively.

Is A Payday Loan A Fixed Loan?

A payday loan is not a fixed loan. It typically involves a fixed fee or interest rate due upon repayment. The loan amount is usually small and due on your next payday, making it a short-term financial solution.

What Is The Major Risk With Using Payday Or Quick Cash Loans?

The major risk of payday or quick cash loans lies in their exorbitant interest rates. These loans can lead to a cycle of debt that’s hard to escape. Borrowers often find themselves needing to take out additional loans to cover previous ones, worsening their financial situation.

Conclusion

Payday loans may seem like a quick solution for financial needs. Yet, their high interest rates and fees often lead to a cycle of debt. Before opting for this type of loan, consider the potential long-term consequences. Exploring alternatives can provide a more sustainable path to financial stability.

Choose wisely to safeguard your future.